Hong Kong Property Looks Good. The Bond Market Disagrees.

Most people entering Hong Kong's property market right now are betting on one thing: that rates stay low. They may want to reconsider.

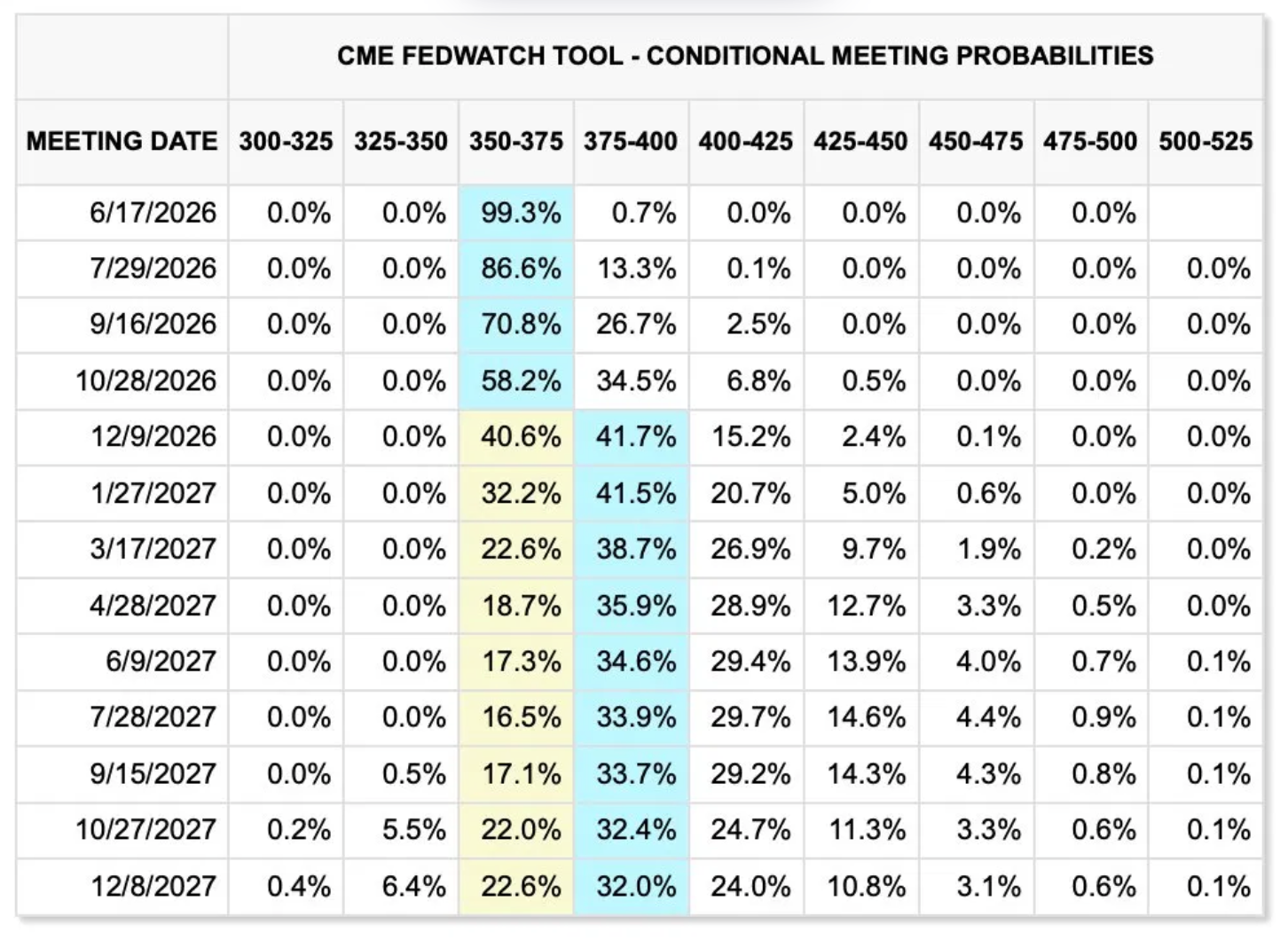

The CME FedWatch Tool tells a story that few buyers are paying attention to. Market pricing shows a growing probability of rate hikes returning as early as September 2026. The 2-year Treasury yield, now above 4.1%, is already pricing ahead of the current Fed Funds Rate of 3.50-3.75%. Historically, when the 2-year yield runs above the policy rate, the Fed follows. The geopolitical backdrop renewed conflict, sticky inflation, and oil prices that refuse to cooperate, only adds to the pressure.

In the late 1990s, the Federal Reserve cut rates aggressively, then reversed course and raised them again. What followed was a financial crisis that reshaped asset markets for years. History does not repeat, but it often echoes.

The Data Does Not Lie

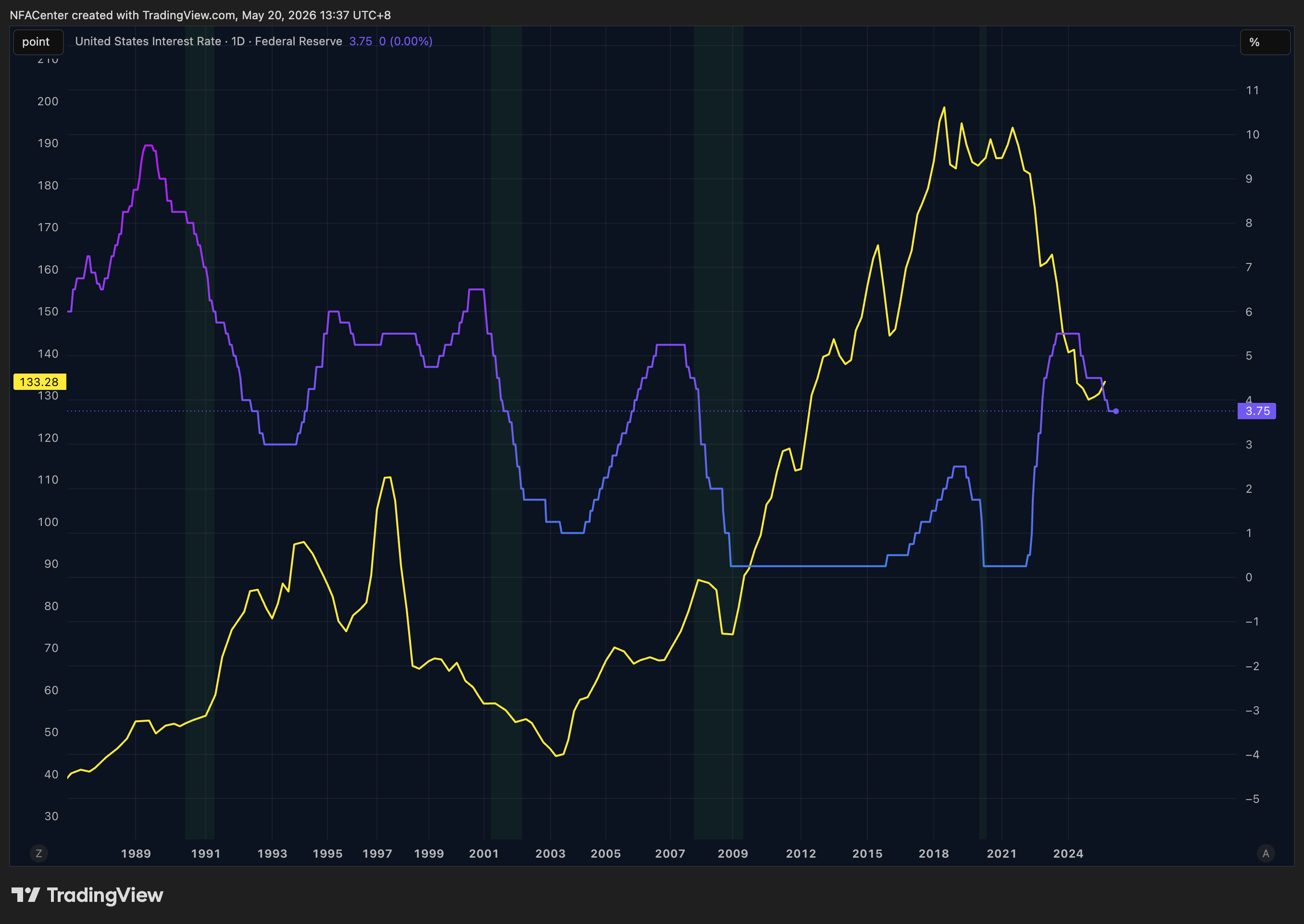

A long-term chart overlaying US interest rates against Hong Kong residential prices tells the story more clearly than any forecast. The relationship is consistent across five decades: when US rates fall, Hong Kong property rises. When rates rise, property falls. The 2008 cycle was the most dramatic illustration, as the Fed cut rates to near zero, Hong Kong residential prices tripled over the following decade. When the tightening cycle began in 2022, prices reversed almost immediately.

With rates at 3.75% and the 2-year Treasury yield already signalling upward pressure, the historical pattern offers a clear warning to anyone expecting a broad-based recovery.

The Summer Window

Headlines are currently positive. Buyers are chasing prices. First-hand private residential registrations reached approximately 5,700 transactions in the first four months of 2026, broadly in line with the historical annual run-rate of around 20,000 units. Sentiment is running warm.

But this is precisely why developers should act now. Many Hong Kong developers are carrying project loans priced at Prime plus 2% or above, directly tied to the lending rate which moves in lockstep with the Fed Funds Rate. Every 25 basis points the Fed raises translates immediately into higher financing costs on unsold inventory. The pressure to sell is not theoretical. It is monthly, compounding, and growing.

The rational move is to release units to market this summer, while buyers are still confident and sentiment remains supportive. Developers who wait risk selling into a weaker environment at a higher cost.

As for whether a wave of simultaneous supply releases will crater prices, that is less a short-term concern than a structural one. The pressure builds gradually. But it builds.

The Supply Problem Nobody Wants to Discuss

Even setting aside the rate question, the structural picture for price appreciation is unfavourable. There are approximately 100,000 residential units in the development pipeline across Hong Kong. That is a fundamental shift in supply dynamics that makes any forecast of double-digit price growth extremely difficult to justify.

Strong demand can absorb supply. But demand being squeezed by higher rates, higher living costs, and cautious consumer sentiment is a different animal entirely.

What This Means in Practice

The residential market is not about to collapse. Structural demand in Hong Kong is real, and the first half of 2026 has demonstrated that buyers with conviction will transact. But the conditions that would drive a broad-based price rally — falling rates, constrained supply, buoyant sentiment are not all present simultaneously, and at least one of them may move in the wrong direction before year end.

For buyers, the calculus is not whether to purchase, but when and at what price. For developers, the priority is velocity over margin. And for anyone watching from the sidelines, the late 1990s parallel deserves more than a passing thought.

Rate cycles have a habit of surprising the people who are most certain they understand them.