Hong Kong Property: Reading the Cycle Honestly

Hong Kong's property market is not just going through a bad patch. The problems run deeper than that, and based on the data, the recovery is still a long way off.

Why Did Prices Get So High?

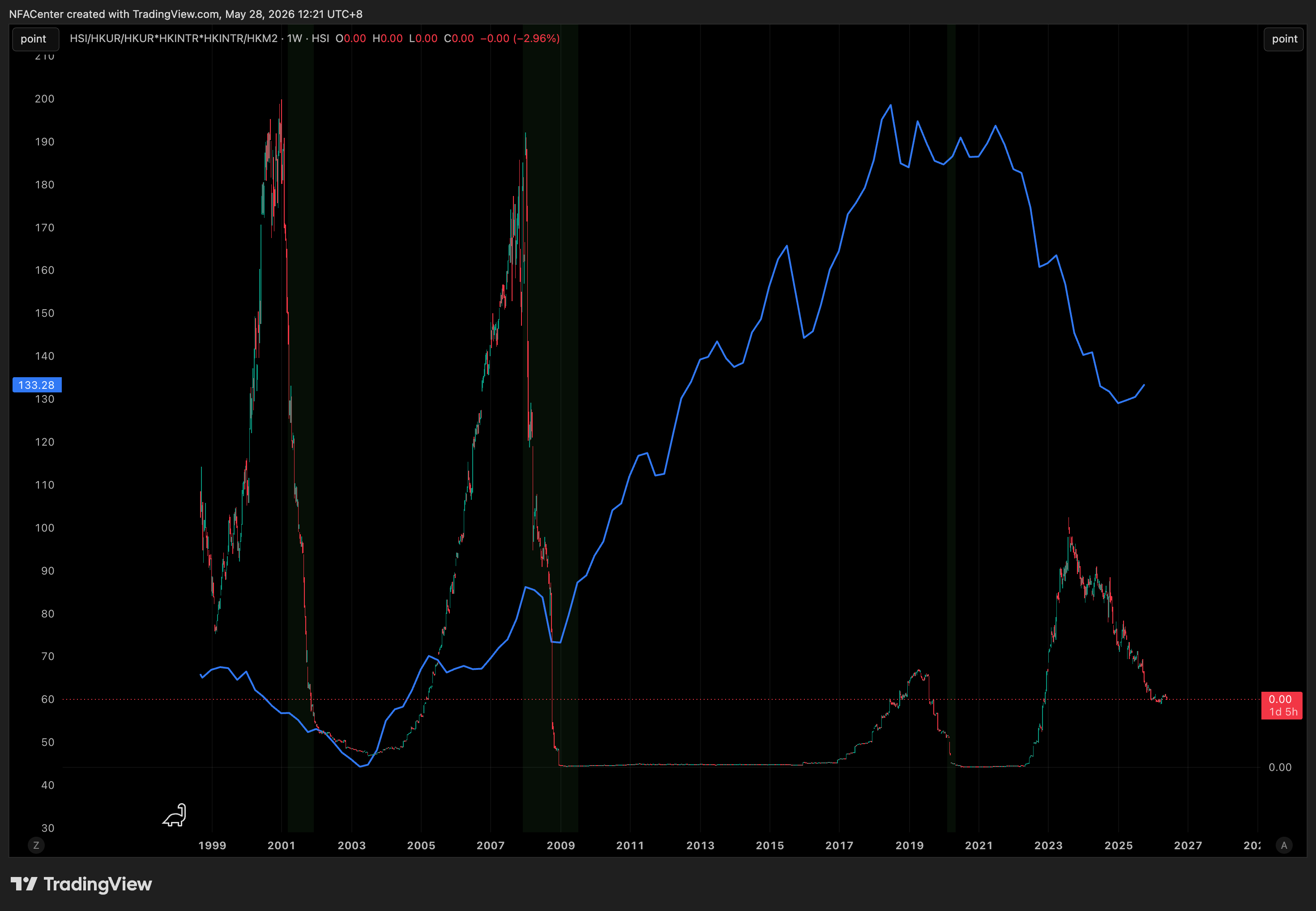

After the 2008 global financial crisis, interest rates around the world dropped to near zero. Borrowing became very cheap. In most markets, this cheap money inflated asset prices without creating real value, a composite index tracking Hong Kong stocks against unemployment, interest rates, and money supply flatlined near zero for over a decade, showing that rising prices were driven by cheap money, not genuine growth.

But Hong Kong property was different. You can print money, but you cannot print land. Limited supply meant that cheap borrowing translated into real price gains. According to BIS data, Hong Kong's real residential property prices nearly tripled between 2009 and 2019, rising from an index level of 65 to a peak of 195.

Where Are We Now?

Since 2019, real property prices have fallen from 195 to 133, a drop of around 30%. That sounds like a lot. But the long-run normal level before all the cheap money was roughly 65 to 80. By that measure, prices have only given back less than half of what they gained. There is still a significant gap to close.

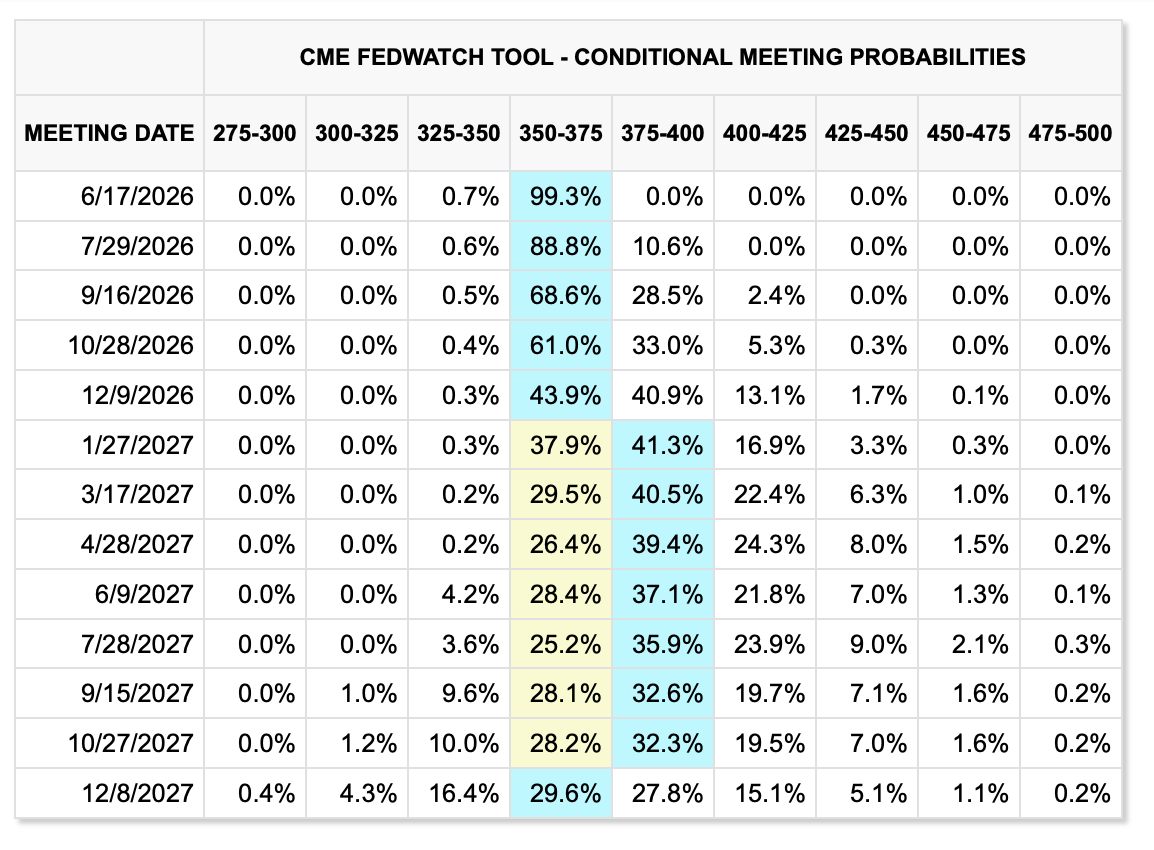

Interest rates are not helping. Markets currently expect US rates to stay around 3.75% to 4.00% through 2027. Since Hong Kong's currency is pegged to the US dollar, local mortgage rates follow. High borrowing costs mean fewer people can afford to buy.

Are Things Getting Better?

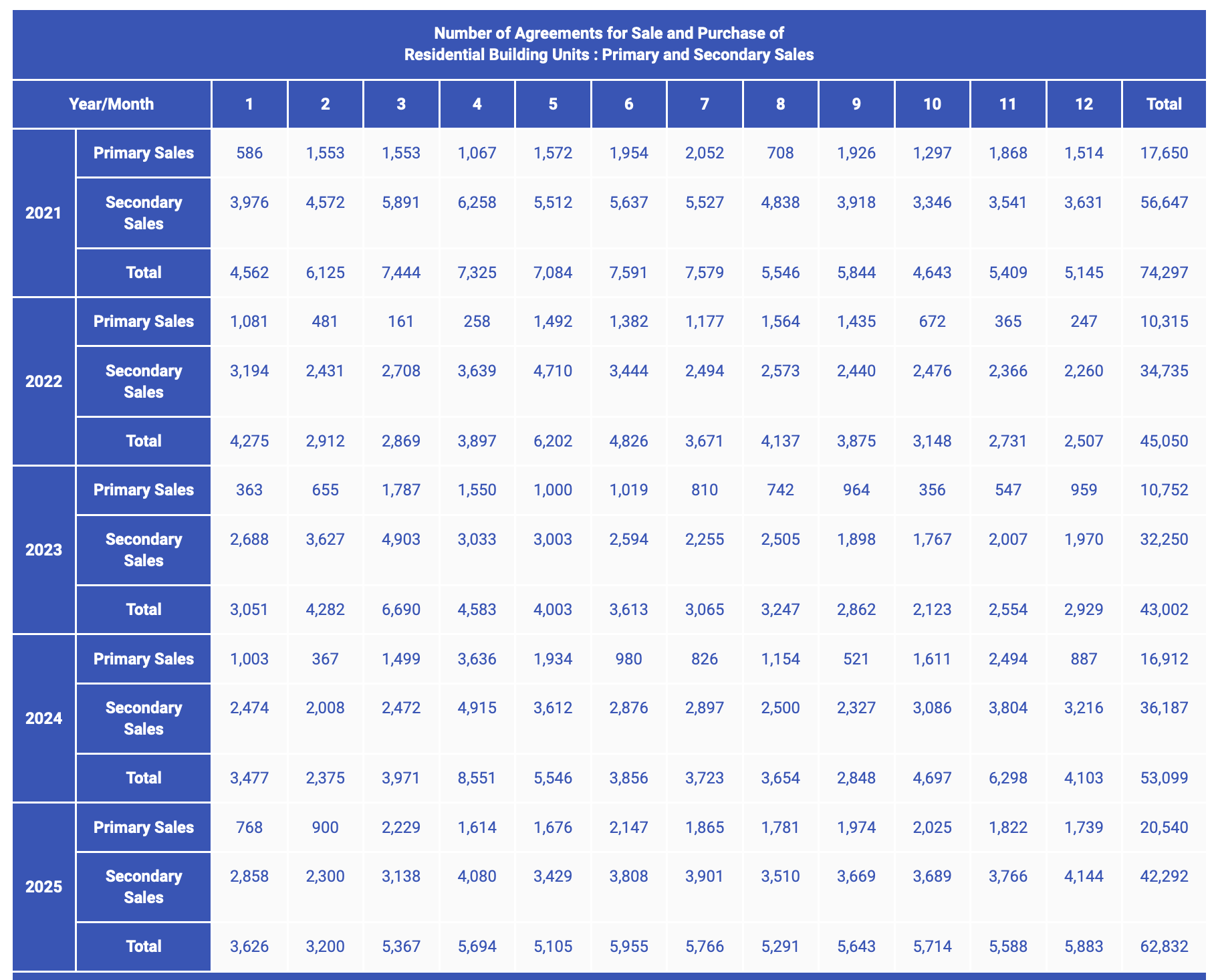

Some signs point to yes. In 2025, first-hand home sales reached 20,540, the best in five years. Total transactions, including second-hand sales, came to 62,832, up nearly 50% from the low point in 2023. People are buying again.

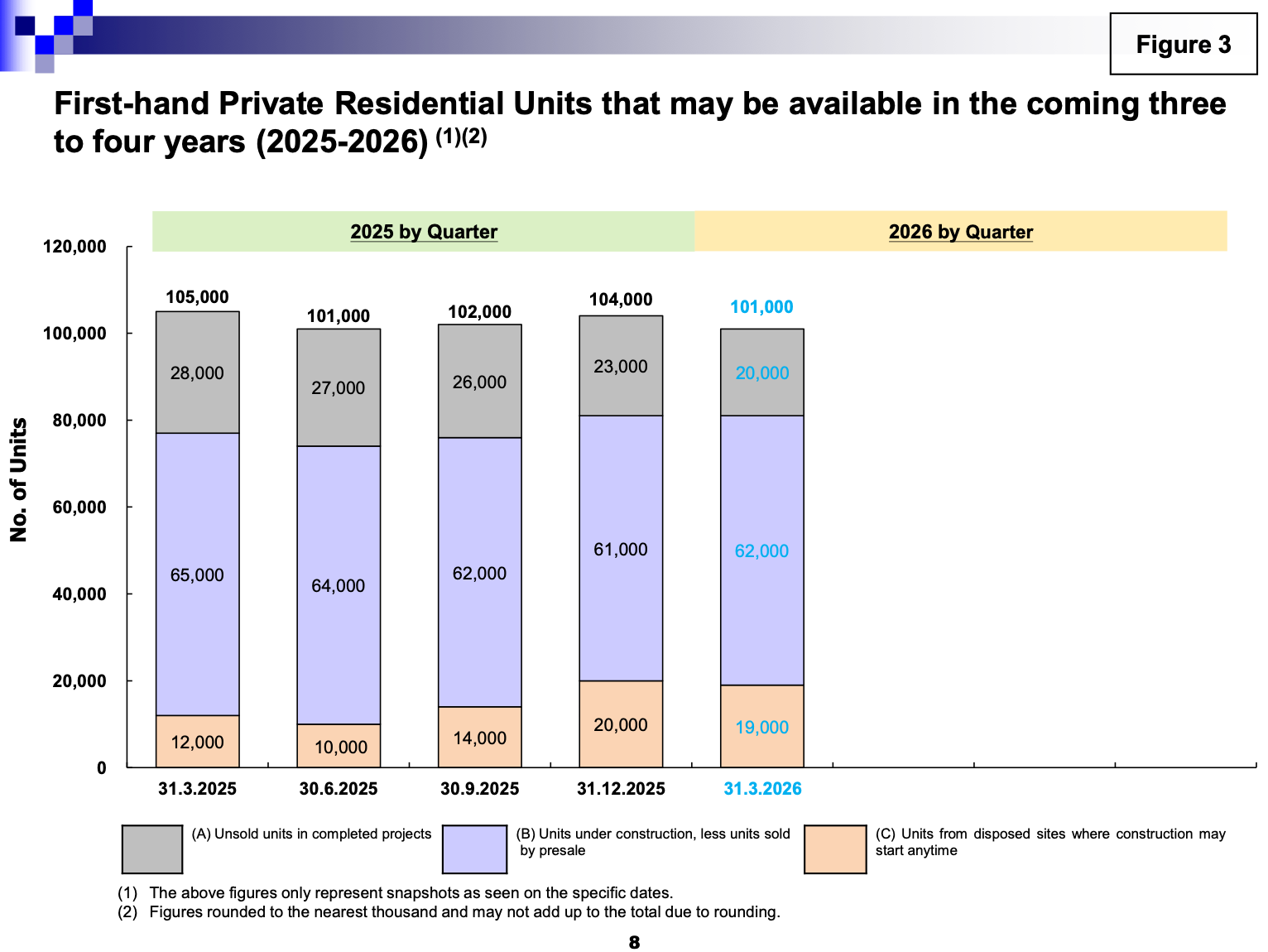

The number of completed but unsold new homes has also been falling — from 28,000 units in early 2025 down to 20,000 by early 2026. Developers are slowly clearing their stock.

But the Supply Problem Has Not Gone Away

Here is the catch. While completed unsold homes are falling at the front end, new supply is building up at the back end. Land that has been approved and is ready for construction jumped from 12,000 units to around 19,000 units over the same period. As old stock gets sold, new supply is lining up to replace it.

The total pipeline of new homes, including units under construction and land ready to build, remains around 101,000 units. At the current buying pace of roughly 20,000 first-hand sales per year, that is about five years of supply. And more keeps getting added.

Think of it like a bathtub. Water is draining from one end, but someone keeps refilling it from the other. The water level barely moves.

Bottom Line

Hong Kong property is caught in a difficult position. Prices are still high by historical standards. Borrowing costs are elevated. And while sales have picked up, the supply pipeline is too large to allow any meaningful price recovery in the near term.

The market is functioning, people are buying and selling. But functioning is not the same as recovering. The structural imbalance between supply and demand has not been resolved. Based on where prices came from, and how much supply is still in the pipeline, Hong Kong has not yet reached exhaustion, but those who understand the cycle will be ready when it does.

As a developer, writing this kind of analysis might seem like an odd thing to do. But I believe that understanding the cycle matters more than looking away from it. A structural correction does not mean the market is finished, it means prices are coming back to reality. And in reality, there are always good projects worth building and good opportunities worth taking. The real question was never "should I buy or not." It was always "at what price, and under what conditions." This article is meant to offer an honest framework not to tell people to walk away.