The Japan Lesson: How Countries Go Broke Without Defaulting

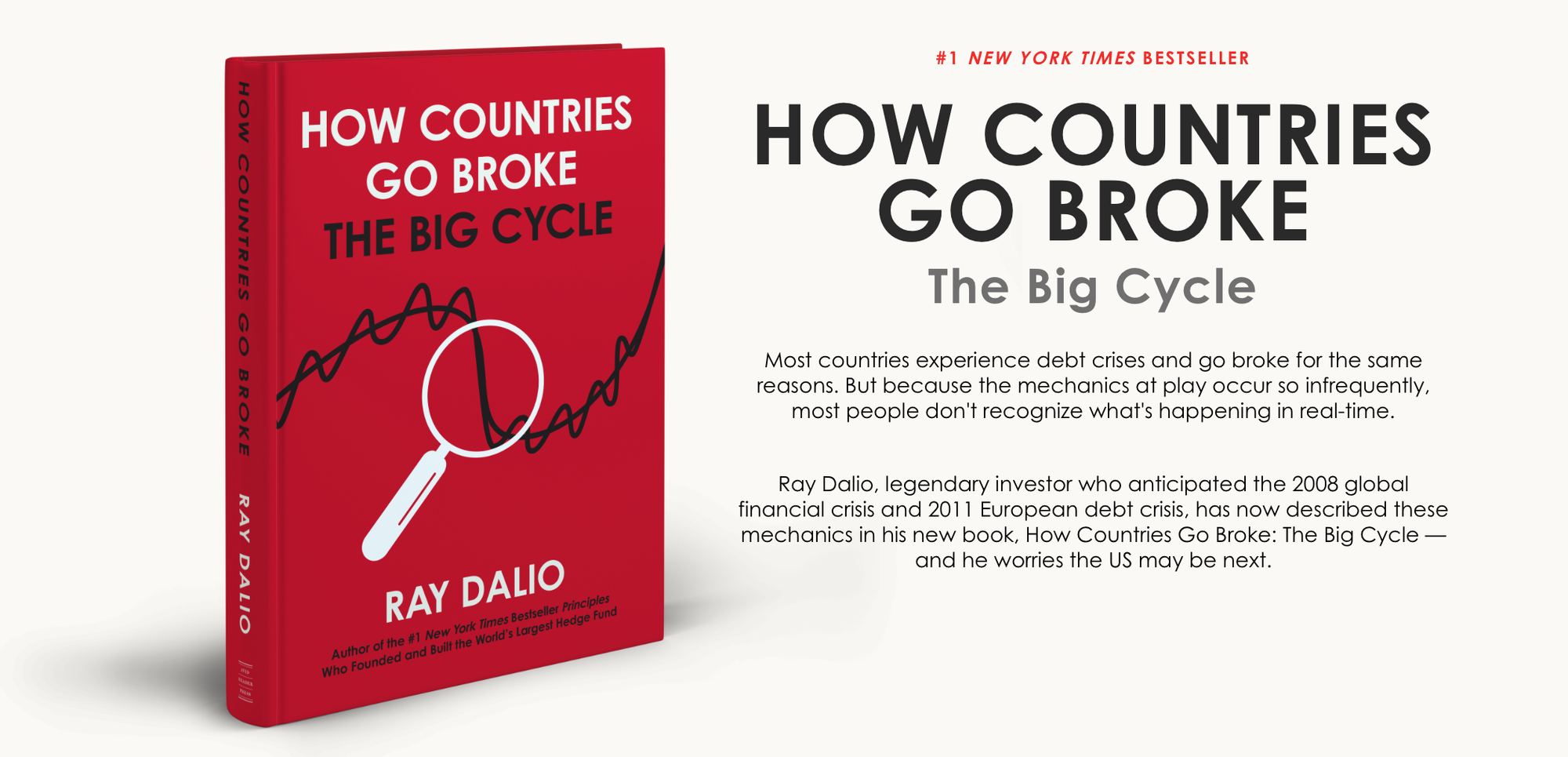

In How Countries Go Broke, Ray Dalio makes an observation that sounds almost paradoxical: countries with printing presses rarely default. They do something quieter instead. They pay their debts in full, in money that is worth less and less.

No missed payments. No dramatic headlines. Just a slow transfer of wealth from savers and workers to the state, spread across decades so that almost nobody notices it happening.

If that sounds abstract, there is a country that has been running this experiment in real time for thirty years. Japan.

The Numbers Nobody in Tokyo Celebrates

Japan never defaulted. Its government bonds remain among the most widely held in the world. On paper, the system worked.

Now look at what happened to the people holding the currency. Japanese nominal wages have barely moved since 1991. Over the same period, South Korean wages grew more than fivefold. Among G7 economies, only Japan and Italy have seen real wages stay essentially flat since 1990, while American real wages rose by half.

Then there is the yen itself. Its real purchasing power has fallen by roughly half over the past four decades. A Japanese saver who did everything right, worked hard, saved in yen, trusted the system, can buy dramatically less of the world today than their parents could.

The government's balance sheet survived. The household's purchasing power paid for it.

How the Mechanism Works

The playbook is not complicated. When debt grows too large to repay honestly, a government with its own currency has three options: default, austerity, or debasement. Default is catastrophic. Austerity is politically impossible. Debasement is quiet.

So central banks hold interest rates below inflation, print money to absorb government bonds, and let the currency slowly bleed. The debt stays technically intact while its real burden shrinks. Bondholders get their money back. It simply buys less.

Dalio calls this the late stage of the big debt cycle, and his argument in the book is blunt: this is not a Japanese anomaly. It is the standard path for every heavily indebted reserve-currency nation in history. The only real variables are timing and speed.

Why This Is Not Just History

Look at where the two largest economies stand today. The United States carries government debt beyond anything seen outside wartime, with structural deficits that neither party shows any intention of closing. China faces its own debt reckoning across property developers and local governments. Both are, by Dalio's framework, deep into the late stage of their debt cycles.

Neither will default. That is precisely the point. The Japanese lesson says the resolution will come the quiet way, through years of money printing, suppressed real rates, and currencies that slowly surrender their purchasing power.

To Be Fair

The dollar is not the yen. It is the world's reserve currency, enjoying structural demand that Japan never had. And America holds cards Japan never held: population growth through immigration, energy self-sufficiency, and a productivity revolution led by AI. If innovation runs fast enough, the United States may simply grow its way out, and the Japanese path is avoided altogether.

But it is worth remembering that UK sterling was once the world's reserve currency too. Reserve status can delay the process. It has never cancelled it. And Dalio's entire argument is that, across five hundred years of financial history, no reserve currency has ultimately escaped.

Where Hong Kong Comes In

For most of the world, this is a story to watch from a distance. Hong Kong does not have that luxury. Our currency is pegged to the US dollar, which means whatever path the dollar takes, we are on it too, without a vote and without the printing press that makes the journey profitable for the issuer.

What that means for this city, and for anyone holding assets here, is a subject that deserves its own discussion. That is where I will pick up next time.