Higher for Longer, Quieter for Now

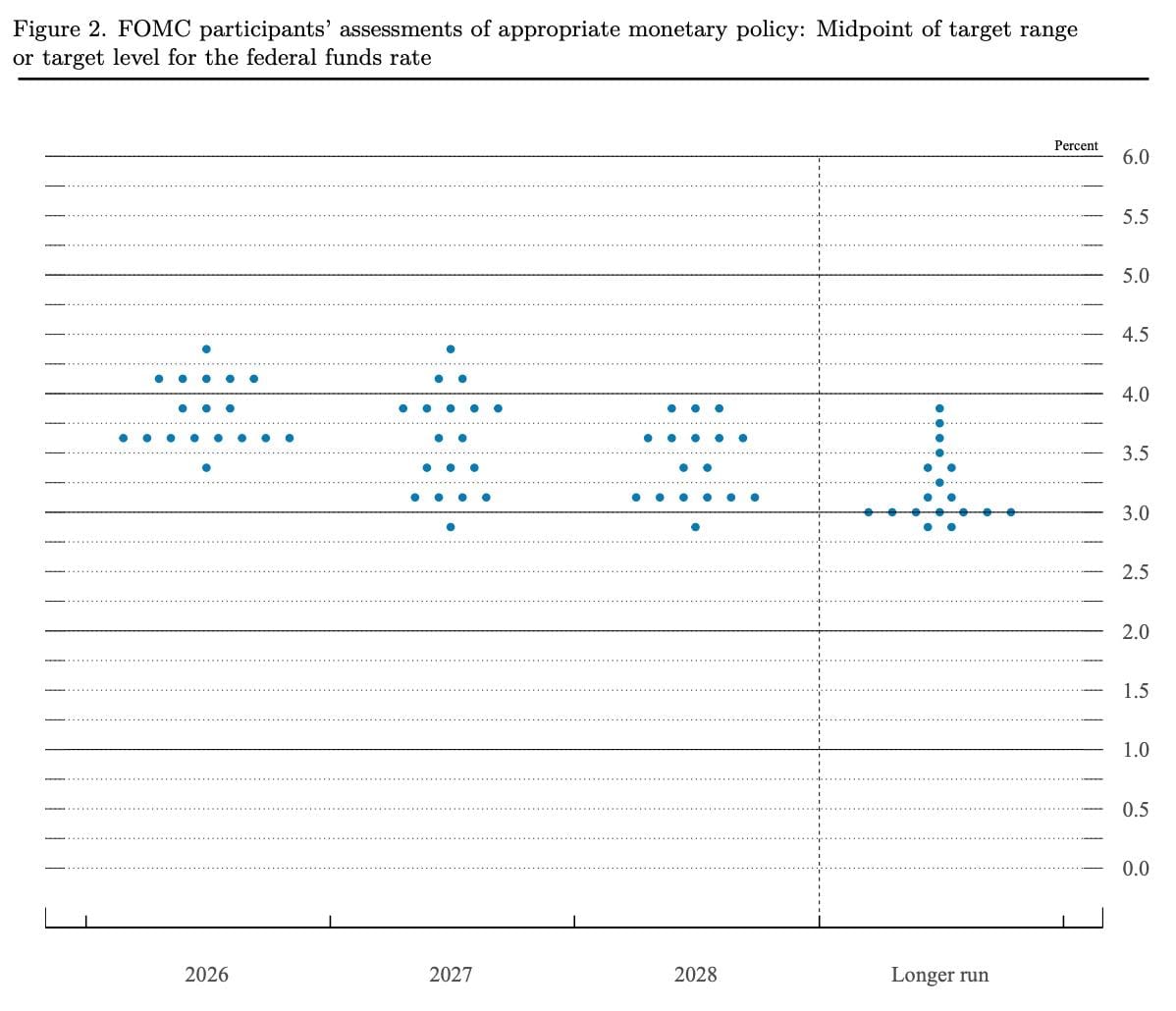

The Federal Reserve held rates steady at 3.5% to 3.75% in June, its fourth consecutive hold. The headline was calm. The detail was not. Nine of the eighteen committee members now project a hike before year end, and the median year-end projection has drifted up toward 3.8%. The era of expecting cuts is, for now, over. The message is higher for longer.

For most markets, that is an abstract policy signal. For Hong Kong, it is mechanical. The Hong Kong dollar's peg to the US dollar means the Monetary Authority has no independent choice. When the Fed holds high, Hong Kong holds high. When the Fed hikes, Hong Kong follows. Every basis point decided in Washington lands directly on local mortgages and developer financing.

The Stock Market Is Already Telling You

You do not need to wait for the property data to see where the pressure is building. The Hang Seng Index has fallen to around 23,500, among the worst-performing major benchmarks in the world this year, while US and Korean indices set records. Property developers listed in the city are trading near multi-year lows.

Equities move faster than property. They are the leading indicator, and right now they are flashing caution. A weak stock market does two things to housing. It erodes the wealth that funds down payments, and it dampens the confidence required to commit to a twenty-year mortgage.

What I Am Seeing on the Ground

Every year, the market quiets as summer arrives. This year is no different, but the slowdown feels familiar in a way that matters. Viewing volumes have dropped. Transactions have slowed. The rhythm echoes 2023, 2024, and 2025, each a year when sentiment cooled before the real test arrived.

Price cutting has not started yet. But my expectation is that it returns toward the end of the third quarter, as developers carrying rate-linked debt grow less willing to hold unsold inventory into a higher-cost winter. From there, I expect Hong Kong property to test another bottom in early 2027. The combination of summer fatigue, elevated rates, and a soft equity market points in one direction for the months ahead.

Why This Is Not a Collapse

Here is where the longer view matters. The Fed's own dot plot suggests rates begin falling by late 2027 and drift lower into 2028. History reinforces the logic. The late 1990s taught the Fed that hiking too aggressively is what triggers the recession it is trying to avoid. Today's inflation is driven largely by geopolitically charged oil prices, a supply shock that higher rates cannot fix, while the real economy is already absorbing strain. The Fed knows this. It will not hike the system into a crisis.

That sets up a turning point. As rates peak and begin to ease, liquidity expectations improve, and the conditions that have weighed on both equities and property slowly start to lift. A market that has spent years pricing in bad news tends to turn well before the news itself turns.

The Bottom Line

The path ahead is not a straight line down. It is a final test of the lows, followed by a recovery as the rate cycle turns, before the next genuine recession eventually resets the board.

For buyers, that makes timing everything. The quiet of this summer, and the price cutting I expect by late this year, may prove to be the window before the turn. The Fed's latest meeting did not just set a rate. It sketched the rough shape of the next two years, and for anyone watching Hong Kong property, the outline is worth studying closely.